Using your car for work changes how insurers view risk. Driving to a single workplace each day is not treated the same as visiting clients, carrying tools or delivering food. The difference is not just wording. It affects underwriting, eligibility and price.

This guide explains how business use is usually categorised in UK car insurance, what insurers typically ask, and where people most often misunderstand the rules.

Social, Domestic and Pleasure vs Commuting

Most standard policies include social, domestic and pleasure use. This covers everyday driving such as shopping, visiting friends or taking children to school.

Commuting is often treated separately. Driving to a single, regular place of work may need to be declared as commuting rather than purely social use. Some policies include it automatically. Others require it to be selected.

If your journey pattern changes, for example moving from working at home to travelling daily to an office, that should usually be updated.

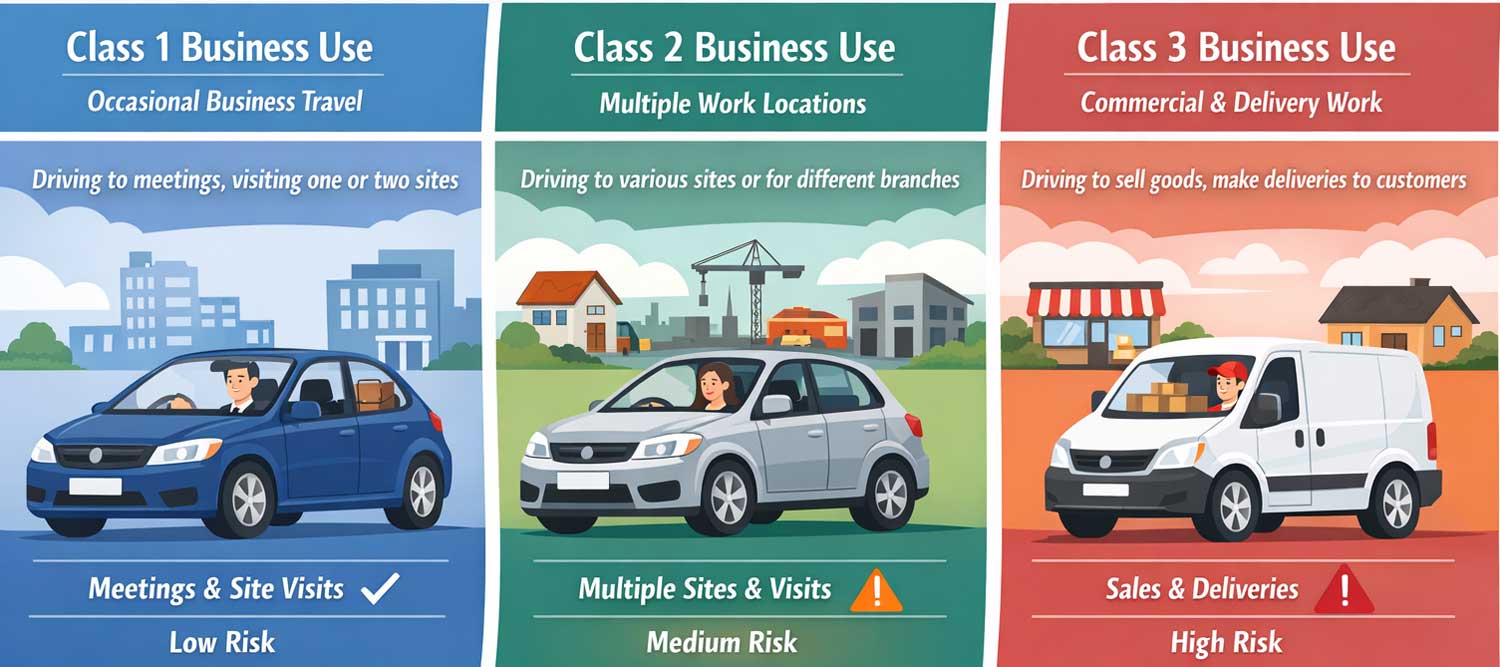

Class 1 Business Use

Class 1 business use typically covers occasional business-related journeys beyond a single commute. This might include visiting clients, travelling between offices or attending meetings at different sites.

It does not normally cover hire and reward work, deliveries for payment or carrying goods for commercial purposes. It is generally intended for low-volume, low-risk business travel.

Class 2 and Class 3 Business Use

Class 2 business use often extends cover to include a named colleague using the same vehicle for business purposes. Acceptance and pricing vary by insurer.

Class 3 business use is usually associated with higher levels of business driving, such as travelling sales roles where the car is used extensively for work. The distinction between classes is set by each insurer’s underwriting rules, so definitions can differ slightly.

Delivery Driving and Hire and Reward

Delivery work and ride-sharing are not normally covered under standard business use classes. Carrying goods or passengers in return for payment is typically categorised as hire and reward.

This includes:

- Food delivery

- Parcel delivery

- Ride-sharing or private hire

Hire and reward insurance is structured differently because time on the road increases significantly and claim patterns differ from ordinary commuting. Trying to insure this activity under standard cover can invalidate the policy.

Using Your Own Car for Your Employer

If you occasionally use your own car for employer-related travel, insurers usually want to know the nature and frequency of that travel. For example, visiting one additional site once a month is different from daily regional travel.

Some employers also have their own insurance requirements. It can be useful to check both employer expectations and insurer terms so they align.

Carrying Tools, Equipment or Samples

Transporting tools or business equipment can increase theft risk and potential claim cost. Insurers may ask whether goods are carried overnight and where the vehicle is kept.

Standard car insurance does not automatically cover the value of tools or business equipment. Separate cover may be required for the contents themselves.

How Business Use Affects Price

Premiums may increase with business use because exposure rises. More time on the road, unfamiliar routes and tighter schedules can all influence risk models.

However, the impact varies widely. Low-mileage, occasional client visits may result in only a modest change, while full-time delivery work can significantly alter pricing and eligibility.

Declaring Business Use Accurately

Insurers rely on the information declared at the point of quote. If your driving pattern changes during the year, it is usually safer to inform the insurer rather than assume existing cover is sufficient.

Misunderstanding usage categories is common. If you are unsure whether your activity counts as business use or hire and reward, clarify before purchasing cover. Adjusting later may involve a premium change or administration fee.

Checking the Policy Wording

Business use definitions are set out in policy documents. These describe exactly what is covered under each class. Because wording varies between insurers, it is worth reviewing the schedule and certificate carefully to confirm the level of use recorded.

If your car use is mainly domestic but occasionally overlaps with work, ensure that overlap is accurately reflected in the policy.

For a broader explanation of how insurers calculate premiums, see What Affects Car Insurance Costs?. For renewals, mid-term changes and switching providers, visit Managing Your Car Insurance Policy.

They are members of the British Insurance Brokers Association, John Stow House, 18 Bevis Marks, London EC3A 7JB; Membership number: 007759.

They are members of the British Insurance Brokers Association, John Stow House, 18 Bevis Marks, London EC3A 7JB; Membership number: 007759.